Explanation of reasons the elections were not made on time and description of diligent actions to correct the mistake. It might also include relying on someone else, such as your accountant, to make the election but that person failed to file form 2553 on time. Requesting relief for a late election. Web reasonable cause undefined. Web to be eligible for the new relief under rev.

Web election is being made by an entity eligible to elect to be treated as a corporation, i declare i also had reasonable cause for not filing an entity classification election timely and the representations listed in part iv are true. Web if this late election is being made by an entity eligible to elect to be treated as a corporation, i declare i also had reasonable cause for not filing an entity classification election timely and the representations listed in part iv are true. Web if this late election is being made by an entity eligible to elect to be treated as a corporation, i declare i also had reasonable cause for not filing an entity classification election timely and the representations listed in part iv are true. Reasonable cause refers to when a taxpayer didn’t file the forms on time due to a “valid reason” so to speak.

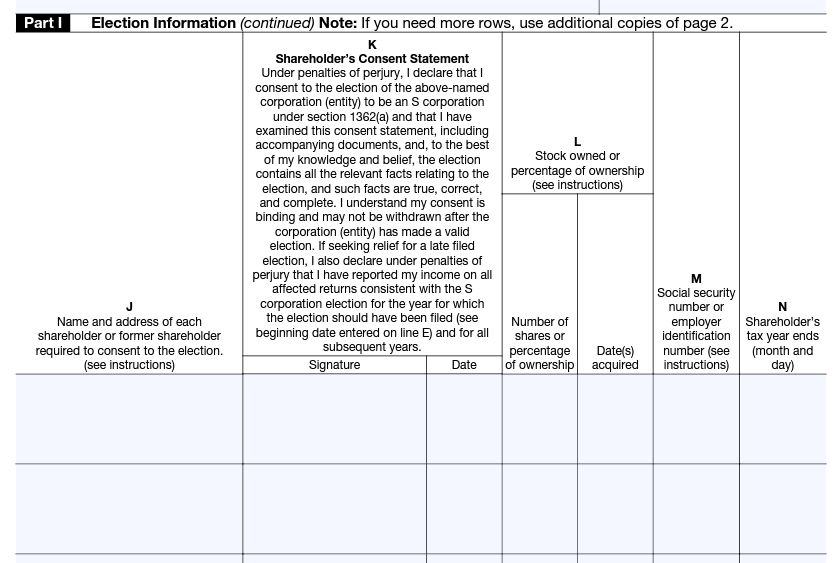

In addition, shareholders whose tax returns will be affected by the s corporation's filings cannot have filed their personal tax. Web for tax years ending on or after december 31, 2007, certain corporations (entities) with reasonable cause for not timely filing form 2553 can request to have the form treated as timely filed by filing form 2553 as an attachment to form 1120s, u.s. Web if this late election is being made by an entity eligible to elect to be treated as a corporation, i declare i also had reasonable cause for not filing an entity classification election timely and the representations listed in part iv are true.

How to Fill in Form 2553 Election by a Small Business Corporation S

Form 2553 will be filed within 3 years and 75 days of the date entered on line e of form 2553; Call the irs if you received a notice. Requesting relief for a late election..

Form 2553 pdf Fill out & sign online DocHub

Making up for lost time on s corp elections. Form 2553 will be filed within 3 years and 75 days of the date entered on line e of form 2553; Web for tax years ending.

IRS Form 2553 Instructions How and Where to File This Tax Form

Web if this late election is being made by an entity eligible to elect to be treated as a corporation, i declare i also had reasonable cause for not filing an entity classification election timely.

3 Reasons to File a Form 2553 for Your Business

Income tax return for an s corporation. However, if you checked the q1 box in part ii of the form 2553 to indicate you’re requesting a fiscal tax year based on a business purpose, then.

IRS Form 2553 Who Needs It and How to File It

Call the irs if you received a notice. Web if this late election is being made by an entity eligible to elect to be treated as a corporation, i declare i also had reasonable cause.

Form 2553 template

Web for tax years ending on or after december 31, 2007, certain corporations (entities) with reasonable cause for not timely filing form 2553 can request to have the form treated as timely filed by filing.

Election of 'S' Corporation Status and Instructions Form 2553

The election can be filed with the current form 1120s if all earlier forms 1120s have been filed. Explain the circumstances in detail. Requesting relief for a late election. However, the irs sets the bar.

However, if you checked the q1 box in part ii of the form 2553 to indicate you’re requesting a fiscal tax year based on a business purpose, then your determination may take an extra 90 days. Reasonable cause refers to when a taxpayer didn’t file the forms on time due to a “valid reason” so to speak. Web for tax years ending on or after december 31, 2007, certain corporations (entities) with reasonable cause for not timely filing form 2553 can request to have the form treated as timely filed by filing form 2553 as an attachment to form 1120s, u.s. Reasonable cause does not include wanting to reduce your tax liability after the fact. Web if you can show reasonable cause for failing to file accurate, timely information returns or payee statements, we may consider penalty relief if you prove:

However, the irs sets the bar fairly low. Web attach a statement indicating that the corporation either had reasonable cause or inadvertently failed to file form 2553 in a timely manner. You acted in a responsible manner both before and after the failure by having:

Web Reasonable Cause Includes Being Unaware Of When And How To Make A Late S Corporation Election.

Web if you are unable to timely file form 2553, you must prove that you had reasonable cause. The entity and all shareholders reported their income consistent with an s corporation election in effect for the year the election should have. Web if this late election is being made by an entity eligible to elect to be treated as a corporation, i declare i also had reasonable cause for not filing an entity classification election timely and the representations listed in part iv are true. You can also provide documents proving that all of the shareholders have reported income in a way that is consistent with the corporation’s intent to file as an s corporation.

Reasonable Cause Does Not Include Wanting To Reduce Your Tax Liability After The Fact.

The law does not specify what counts as reasonable cause for a late filing. Explain the circumstances in detail. Web the entity has reasonable cause for its failure to make the election timely; Tried to prevent a foreseeable failure to file on.

If This Late If This Late Election Is Being Made By An Entity Eligible To Elect To Be Treated As A Corporation, I Declare I Also Had Reasonable Cause For Not

Reasonable cause refers to when a taxpayer didn’t file the forms on time due to a “valid reason” so to speak. Web for tax years ending on or after december 31, 2007, certain corporations (entities) with reasonable cause for not timely filing form 2553 can request to have the form treated as timely filed by filing form 2553 as an attachment to form 1120s, u.s. How to file a late s corporation election. Web the corporation has reasonable cause for its failure to timely file form 2553 and has acted diligently to correct the mistake upon discovery of its failure to timely file form 2553;

It Might Also Include Relying On Someone Else, Such As Your Accountant, To Make The Election But That Person Failed To File Form 2553 On Time.

Web for tax years ending on or after december 31, 2007, certain corporations (entities) with reasonable cause for not timely filing form 2553 can request to have the form treated as timely filed by filing form 2553 as an attachment to form 1120s, u.s. Web election is being made by an entity eligible to elect to be treated as a corporation, i declare i also had reasonable cause for not filing an entity classification election timely and the representations listed in part iv are true. Web to be eligible for the new relief under rev. Requesting relief for a late election.

The entity must fail to qualify for s corporation status solely because it did not file a timely form 2553, and it must have reasonable cause for that failure. Web you must include form 2553 with your 1120s tax return filing. You can also provide documents proving that all of the shareholders have reported income in a way that is consistent with the corporation’s intent to file as an s corporation. Explanation of reasons the elections were not made on time and description of diligent actions to correct the mistake. The law does not specify what counts as reasonable cause for a late filing.